Three million two hundred and seventy-six thousand nine hundred and forty-eight (3,276,948), this is not a random number but the number of years that Elon Musk, founder of SpaceX and Tesla, can survive in the future if he spends the average American salary of $56,516 per year.

If you are able to save an unrealistic 50% of your income and stash it under the mattress every year it would take you 6.5 million years to save your way to Elon’s wealth, okay I get it. So we can’t all be the richest people on the planet, but what about a million dollars? Surely it can’t be that difficult, right?

Well, let’s say you’re an average engineer earning eighty thousand dollars ($80,000) per year. It would take 16 years just to earn one million dollars. However, that doesn’t include rent, food, and the cost of living. If you diligently and consistently save 10% of your earnings, it would take 156 years to save your way to a million dollars. For the average teacher, it takes 217 years, and for a bartender, it takes 625 years. You see, for rich people, wealth is measured in time.

Suppose if you lose your job tomorrow, how many days, months or years can you survive on your savings, that is the definition of wealth. So how long can you survive?

This book gives you the financial intelligence that you probably missed out on growing up the secret Financial intelligence that wealthy families pass on from generation to generation. The education system and your parents never gave you this information, and that is why so many people are forever stuck in the rat race.

After reading the book summary of Rich Dad Poor Dad you will know 95% of everything. This book helps you explain all the most important concepts that will change your perception of wealth and guide you on your journey to Financial freedom.

The Story Of Two Fathers

“Rich Dad, Poor Dad” by Robert Kiyosaki explains the financial philosophies of two influential father figures in the author’s life. The first father referred to as the “Poor Dad,” was a well-educated man who followed the traditional path of getting a good education, working for a stable job, saving money and being careful with spending.

While, the second father, known as the “Rich Dad,” was a self-made entrepreneur who believed in financial education, investing in assets, and creating multiple sources of income. These two fathers have very different ideas about how to be successful with money, and that’s what the book is all about.

Lesson One

The Rich Don’t Work For Money

Robert Kiyosaki, the author of this book, learned a big lesson about money when he was just 9 years old. He and his friend Mike asked Mike’s dad, who they called ‘Rich Dad,’ how to make money. Robert was upset about earning only 10 cents a week, which seemed like very little money. He thought about quitting his job every week when he saw how little he was paid. It was at this moment that ‘Rich Dad’ taught them their first lesson about money. He explained that while poor and middle-class people work for money, rich people make money work for them.

One of life’s biggest traps “The Rat Race”

Two powerful emotions, fear and greed, often control our lives. It begins with the fear of not having enough money, pushing us to work harder. As paychecks start rolling in, our desire for new cars, gadgets, shoes, and clothes increases.

We want more things, so we work harder to get promoted, and then the pattern is set and we are stuck in it. We wake up, go to work, and pay the bills.

The more we earn, the more we spend, and this keeps us trapped in a cycle called the “Rat Race”. To change this nine-to-five mentality driven by fear and greed, Robert and his friend started working only for knowledge. Rich Dad challenged them to find ways to generate their own income.

They finally came up with the business idea when they discovered some old comic books at one of Rich Dad’s stores. They decided to create their own library in the basement, charging their classmates 10 cents for admission. This idea allows them to earn $9.50 per week without much effort.

Key Lesson

Getting a job is really just a short-term solution to building your net worth because the more you earn the more you spend, this is human nature and it is driven by fear and greed. You are forced to work for someone else for the rest of your life if you get stuck in this cycle.

To escape this cycle, focusing on knowledge and creating opportunities for generating income can provide a way out, as demonstrated by Robert and his friend’s clever idea of starting a basement library.

Lesson Two

Why teach financial literacy?

If you think school can make you rich, you`re looking in the wrong place. The education system’s main objective is to train you on how to become a good employee but it does not make you a good employer. Things like personal finance management and wealth building are not taught in the current education system.

You cannot depend on others to help you use that knowledge and acquire assets that allow you to generate income. Understanding the difference between an asset and a liability is the first pillar of financial literacy and escaping the rat race.

Difference between Asset and Liability

A liability takes money out of your pocket while an asset puts money into your pocket. Income represents the money that you earn, and expenses are the money you pay for things like rent, food, electricity, and clothing. An asset is something that enables its owner to make money, whereas a liability is something that costs money.

Rich people acquire assets and the poor and middle class buy liabilities that they think are assets.

Cash Flow Patterns

How someone handles money is called “cash flow”. Let’s look cash flows of different classes.

Cash flow of a poor person

They have a job get a salary, and use all their salary on expenses and they usually live from paycheck to paycheck.

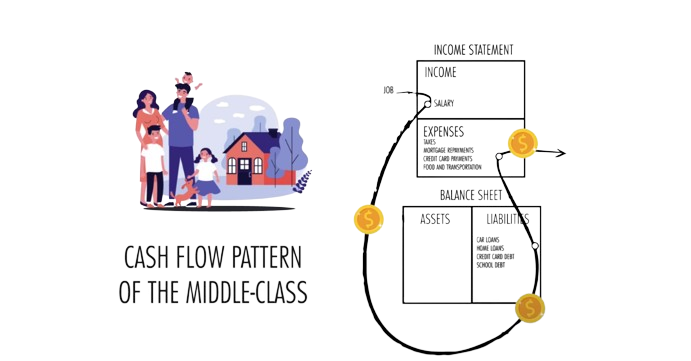

Cash flow of the middle class

They have jobs receive a salary but most of their money is spent on liabilities and expenses like home loans, car loans, debt or credit cards, mortgage payments and taxes. They think that their house is an asset but one day they wake up with a lot of mortgage and credit card debts.

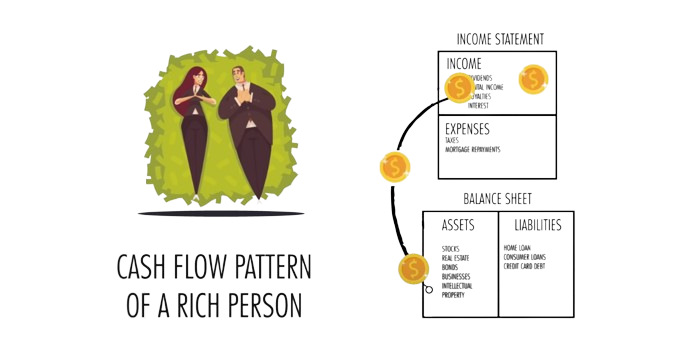

Cash flow of a rich person

The rich always think of ways to grow their assets. Assets they acquired over time, are their main source of income.

Your home is not an asset

Focusing on buying a house can be financially challenging because it takes many years to repay the loans and property taxes. And also your home`s value may not always go up due to the different expenses. But the real problem is missing out on the other investment chances.

When you put your money into a home and spend it on mortgage payments, you miss out on opportunities to grow your investments elsewhere. Don`t forget about the many other investment options besides just local real estate.

Some examples of real assets

Repayment of the property loan can be done using the tenant’s monthly payments. A business that does not require your presence inside. For Poor Dad, the house is an asset, and for Rich Dad, the house is a liability. Most people fall into this trap because they don’t understand the difference between an income statement and a balance sheet.

Why people struggle

This is what your life will become if you follow the crowd. You work for three people.

- You work for the company to earn your salary but at the same time, you are making the owner and the shareholders rich.

- If you are in debt, you will work for a bank. Banks make a lot of money from your interest payments.

- And finally, you work for the government. The government will cut off your money before you even see it. Working more means paying more taxes.

Take a calendar year, if you are a regular person, every dollar you earn from January 1 to March 16 goes directly to the government, that is two and a half months every year you pay to the government, compounded over 40 years that is almost six years just to pay taxes to the government. Rich people understand this, but common people do not.

Ways to get out of the Rat Race

Understand the difference between assets and liabilities. Focus on acquiring assets that generate money. Reduce your expenses and debt as minimum as you can. And just saving money doesn’t exclude anyone from the Rat Race. Save money and invest it to increase your income.

Key Lesson

Life is not about how much money you earn but how much money you save. The key to achieving this is having the financial knowledge to understand the difference between assets and liabilities. Unfortunately, the middle class has liabilities that they mistakenly consider assets.

Lesson Three

Mind your own business

The rich focus on their assets while common people focus on their income statements. Robert’s first professional job was far from glamorous. He was a photocopier salesman for Xerox. After three years, the income from his investments surpassed his salary because he had invested in apartments. It was then time for him to leave Xerox and look after his business full-time. So, what assets can you focus your attention on?

- Businesses that do not need your presence to operate.

- Stocks.

- Bonds.

- Income generating from real estate.

- Notes or IOUS.

- Royalties from the intellectual properties such as movies, music, scripts, or patents.

- Anything that produces an income or appreciates in value things like cryptocurrencies, websites, YouTube channels Etc.

Don’t let a dollar come out from your asset again. Grow your assets. Robert thinks about every dollar he invested in his assets as an employee because money can work for 24 hours a day.

Key Lesson

Don’t confuse your profession with your business. The middle class focuses on their profession and as a result, they spend their entire lives building other people’s businesses while the rich focus on building their own businesses. Your job deals with the income part of your finances, while your business is all about the assets.

Copy Link

Copy Link